Ulta Is An Attractive Investment - Ulta Beauty, Inc. (NASDAQ:ULTA)

Investment Thesis

Ulta Beauty (NASDAQ:ULTA) is an attractive investment opportunity that will only increase in value as it continues to expand both online and in brick-and-mortar stores. A significant increase in the company e-commerce sales, as well as in-store sales, is a positive sign that it is able to keep up with the changing environment of retail as more of them move further online. At a current price of $251 and a 52-week high of $315, I expect Ulta to climb back to those levels and exceed them in the coming year. Looking ahead to the company's Q2 earnings report on August 24, it is expected to have increased levels of inventory from August through November as it begins to prepare for the holiday season. This may be a good time to purchase Ulta if investors see the increase in expenses and don't look further into the reasoning behind it.

Overview

Ulta Beauty is the largest beauty retailer in the United States and the premier beauty destination for cosmetics, fragrance, skin care products, hair care products and salon services. It offers a unique combination of more than 20,000 beauty products across the categories of prestige and mass cosmetics, fragrance, haircare, skincare, bath and body products and salon styling tools, as well as a full-service salon in every store featuring hair, skin and brow services. The company focuses on delivering a compelling value proposition to guests across all product categories as well as convenience, as its stores are predominantly located in convenient, high-traffic locations. With over 1,000 stores in almost every state, Ulta has been able to spread its brand all over the US.

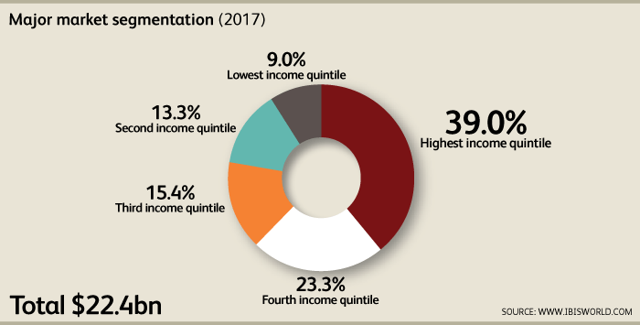

Trends

Ulta operates in the beauty, cosmetics, and fragrance industry. This industry is undergoing 5.1% growth and is expected to decrease slightly to 4.5% over 2017-2022. Ulta makes up 23.1% of the total market share of this industry, with L Brands (NYSE:LB) and Sephora (OTCPK:LVMUY) behind it.

(Source: IBISWorld)

Consumers are increasingly flocking to beauty retailers such as Ulta, as they offer product expertise and loyalty programs. Product expertise is something that continues to attract customers new and old despite the rise of beauty e-commerce, and is one advantage that Ulta has over competitors like Amazon (NASDAQ:AMZN) that sell similar products online. The expanding U.S. beauty products and salon services industry and the shift in distribution channel of prestige beauty products from department stores to specialty retail stores will continue to fuel the growth of companies like Ulta.

An increase in disposable income has also helped improve sales in this industry and will continue to drive the premium range of products that are offered along with their higher margins. Profits of these companies are expected to rise from 6.2% to 7.4% in 2017 as the economy continues to grow.

Beauty retailers are also beginning to expand their target markets towards teenagers and men, as the male grooming market is projected to reach $60.7 billion by 2020. Furthermore, brick-and-mortar accounts for over 80% of male grooming product sales globally. Ulta is set to take advantage of this, as the majority of its sales come from its brick-and-mortar stores.

Financials

Ulta saw its net sales grow by 22% in its most recent quarter - a strong sign that the company is handling transitioning more of its business online well. Most of this growth has been driven by new store openings and the increase in its e-commerce sales. Comparable sales also increased 14%, resulting from 8.7% increased traffic and a 5.6% increase in average tickets. Ulta has been to turn its sales into profits too: net income rose by 39.4%. Due to the sales of more high-end products and services, the company has been able to maintain a fairly wide profit margin compared to the industry of 8.75%.

Ulta's cost of capital is 6.02% and it has an ROIC of 40.11%. This is a good sign that the money that it uses is going to the right places, and the company has attributed much of its success to its marketing and merchandising strategies. With no debt and enough cash to sustain itself, Ulta is in a strong financial position going forward.

Threats

Loyalty member transactions make up more than 90% of its annual net sales. The good sign is that customers enjoy shopping at Ulta and continue returning as the company offers members exclusive discounts and promotions, but I fear that it may become too reliant on its members. Competition has been tough, coming from online retailers such as Amazon and Target (NYSE:TGT) to smaller specialty stores like Mr. Porter (OTCPK:YXOXY) and The Art of Shaving (NYSE:PG). It's not hard for another company to undercut it in price or by offering promotions on similar products, and they can take away market share from Ulta.

Ulta has e-commerce sales of approximately 7% as of January 28, 2017, and expects it to grow to approximately 10% of total sales by the end of fiscal 2019. While the company has seen e-commerce sales increase 71% year over year, much of its business is from its brick-and-mortar stores. As more people begin to move their shopping online, the company may not be moving fast enough in order to capitalize on the online beauty market.

Ulta relies on the economy and disposable income to generate its sales. People aren't going to prioritize cosmetics and premium salon services if unemployment is rising and interest rates keep climbing. In the event of a prolonged economic downturn or acute recession, consumer spending habits could be adversely affected and Ulta could experience lower-than-expected net sales. Rising geopolitical risks could see a material impact on the business, especially with tensions between the US and the Korean peninsula rising.

Ulta competes across a range of markets: regional and national department stores, specialty retailers, drug stores, mass merchandisers, high-end and discount salon chains, locally owned beauty retailers and salons and e-commerce businesses. Competing companies may have greater resources to market their brand or adopt aggressive pricing policies to drive down their market share. Local beauty retailers may also take some sales away, as they can specialize in certain areas that Ulta cannot due to its size.

Conclusion

Despite all these threats, Ulta has proven quarter after quarter that it can continue to grow, and looking over its financial statements I begin to see why. The company's expertise in its area, along with its in-store services, help drive consumers into the stores. An experience like this can't be replicated online, and consumers still see value in shopping in-store. While much of the world continues to move online to do their shopping, so does Ulta. With e-commerce sales up by 71% compared to the previous year, the company has done a good job at making the transition from brick-and-mortar to online without sacrificing sales. We can expect to see Ulta continue to grow at its current rate if market conditions hold up and risks remain low.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments

Post a Comment